Reflecting on CSRD DAY: the upside of making impact reporting optional (again)

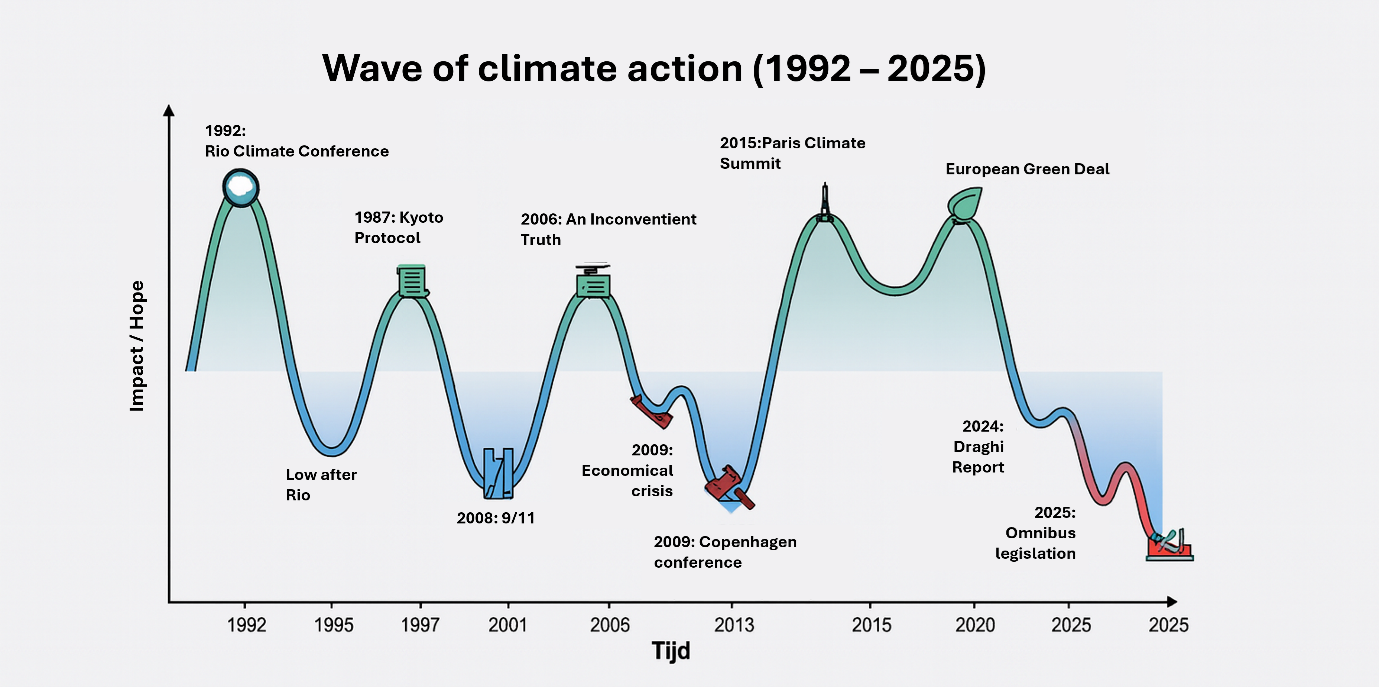

With strong keynotes, two deserved winners, and a day full of energising conversations, it’s hard to pick one takeaway from CSRD Day. One moment that stayed with me was Fu-Khan Tsang’s observation that movements come in waves – and that sustainability (and sustainability reporting) is no exception. Every high in climate action, he argued, has been followed by a low. His conclusion was grim: we’re currently at an all-time low.

I understand how he got there. But a low can also be a turning point. And if we look closely, this may be the moment to create the conditions to deliver real impact. Let’s unpack why.

Figure 1: The wave of climate action. Modified from Fu-Khan Tsang’s presentation at CSRD Day

Figure 1: The wave of climate action. Modified from Fu-Khan Tsang’s presentation at CSRD Day

The “wave” Tsang described aligns with my own experience. When True Price was founded in 2012 (and when I joined in 2015), people told us what we were doing was impossible. I still remember hearing: “Great idea, but you do realise this will never happen, right?” We kept going anyway. And it did happen.

At first, change came slowly and steadily. We worked with frontrunners willing to experiment and to publish their true prices. Only a few years later, the first true price supermarket opened. Today, multiple academic groups across Europe work on true pricing, and the FAO has published its State of Food and Agriculture on true cost accounting twice in a row. What once sounded unrealistic has become increasingly mainstream.

In parallel, we saw the rise of impact reporting. The first reports were voluntary – and precisely because they were voluntary, they often had real transformative power. One of our early clients was at CSRD Day. He laughed as he recalled he almost had to trick his CFO into publishing their first impact report. But by year two, this CFO was the biggest advocate.

In Tsang’s picture, these breakthroughs happened near the highs of the Paris Agreement and the European Green Deal: years when the world was unusually receptive to ambitious ideas. Out of the Green Deal came the CSRD. Much of what we had been doing voluntarily with companies suddenly became mandatory.

I had mixed feelings about that shift. On the one hand, I’m proud of the hundreds of professionals we trained through CSRD-in-one-day. And I’ve learned that compulsory disclosure can be a powerful trigger to improve: few organisations want to publish the same negative impacts year after year without showing progress.

On the other hand, we also saw many companies move into a “compliance-first” mindset. Teams poured their energy into filling hundreds of pages. Clever and genuinely transformative initiatives were postponed – because the priority became getting the report out, not changing what the report describes. So, I began to wonder: was this a true high point of climate action – or were we mistaking activity for progress?

Then the backlash came. This culminated in the Omnibus proposal earlier this year. It’s easy to see why Tsang calls this a low point: CSRD is set to become only for the largest companies (92% reduction with respect to the original scope) and the proposed depth of analysis is much, much less (70% fewer datapoints than in the original scope).

But here’s the contrarian take: this moment also creates an opening. Fewer companies in the formal CSRD scope means many can opt for the Voluntary SME standard, which is genuinely solid. And often it is better suited to where all but the largest companies are today.

Fewer compulsory datapoints can mean more room for a coherent narrative, clearer priorities, and the capacity to think beyond checklists. That capacity can be used for the work we pioneered before CSRD: valuing impacts in monetary terms so trade-offs become visible; focusing on what is objectively most material; and using impact information not only for reporting, but for decision-making, strategy, and financial systems.

In a way, we may even be better positioned than before CSRD existed. The expertise has grown – both in sustainability and reporting teams and at the board. The conversation has moved forward. There is still political capital, it just needs to be channelled to change instead of compliance.

So yes: we have gone up and down. But we’re not back at zero. The question is whether we use this moment to retreat into minimal compliance, or to return to what works: using impact measurement as a management tool, and impact reporting as a lever for change.

Now we just need to do it.